The Strategic Center of Excellence: How Banks Secure AI Sovereignty

Most banks today are running dozens of AI pilots. Few can scale them.

Fraud teams train their own models. Customer units experiment with chatbots. Risk divisions contract new vendors. What emerges is not transformation but fragmentation: duplicated costs, uneven standards, and compliance exposures regulators will no longer tolerate.

The question is not whether banks adopt AI. That debate ended years ago. The question is how they institutionalize AI without losing clarity, compliance, or client trust.

The only credible answer so far is the Center of Excellence (CoE).

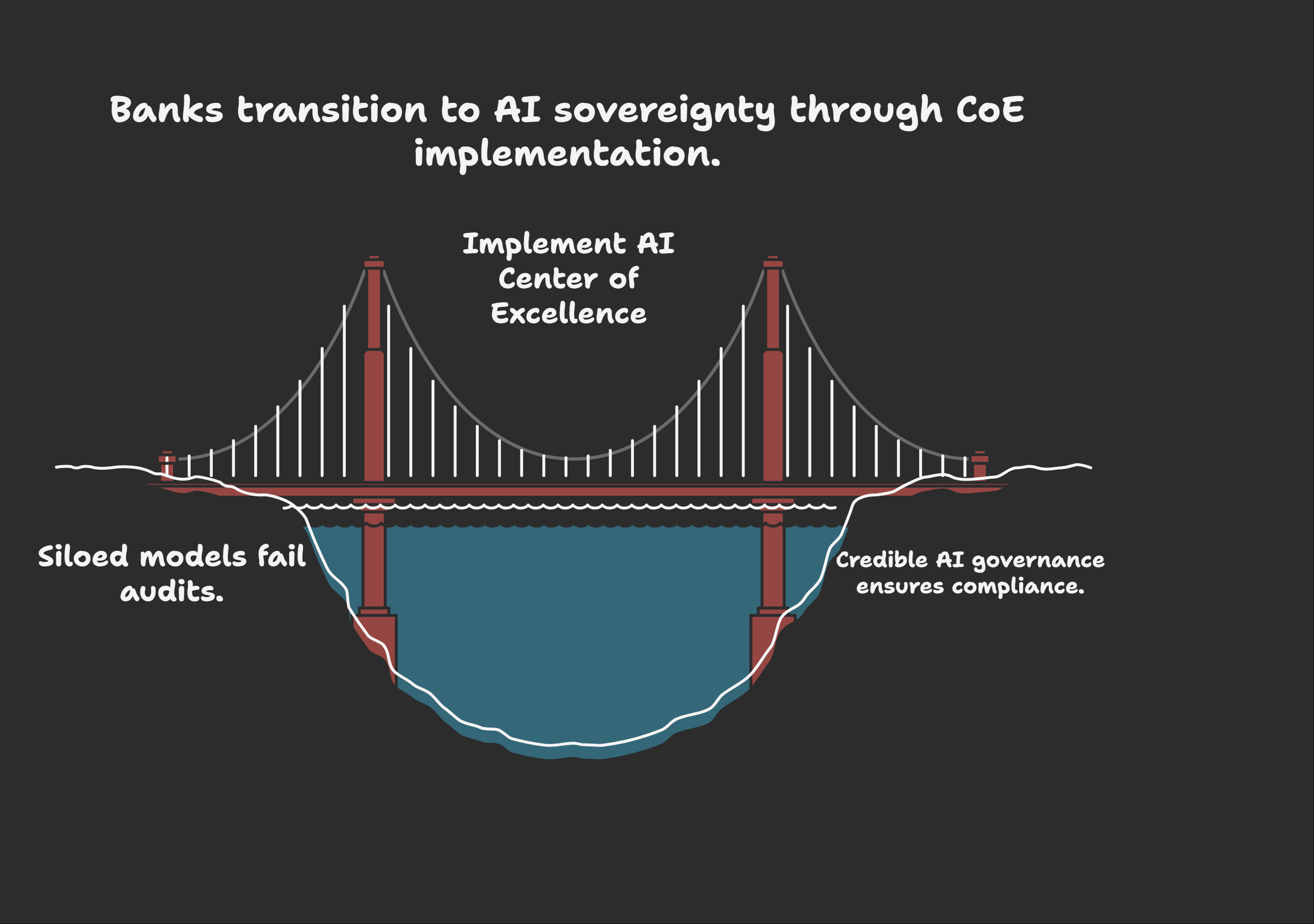

The Regulatory Cliff

By 2027, CRS 2.0 and CARF will be fully enforced across 51 jurisdictions. The schemas are already published. The deadlines already signed. Crypto, e-money, enhanced due diligence — all non-negotiable.

For institutions that still treat AI as scattered experiments, the danger is real: models built in silos will fail the audit trail. Compliance obligations cannot be met by fragmented initiatives. Regulators will expect enterprise-level governance.

In other words: no CoE, no credibility.

ING: From Experimentation to Sovereignty

Europe’s ING Bank provides the most decisive case study.

By centralizing its AI strategy into a single Center of Excellence, ING created an institution-wide hub that pooled data scientists, risk officers, and compliance experts. The outcomes were immediate and structural:

Scalability: Risk and fraud models scaled across markets in months, not years.

Regulatory Alignment: Supervisors recognized the CoE as a governance anchor, with explainable, auditable models.

Operational Consistency: Every market hub operated on the same standards.

The CoE became the difference between scattered pilots and institutional sovereignty.

Contrast this with banks that placed AI inside “innovation labs.” Most prototypes never left pilot stage. Without central authority, dozens of projects multiplied — none built for regulatory audit, none achieving enterprise ROI.

The lesson: discipline, not demos, defines AI leadership.

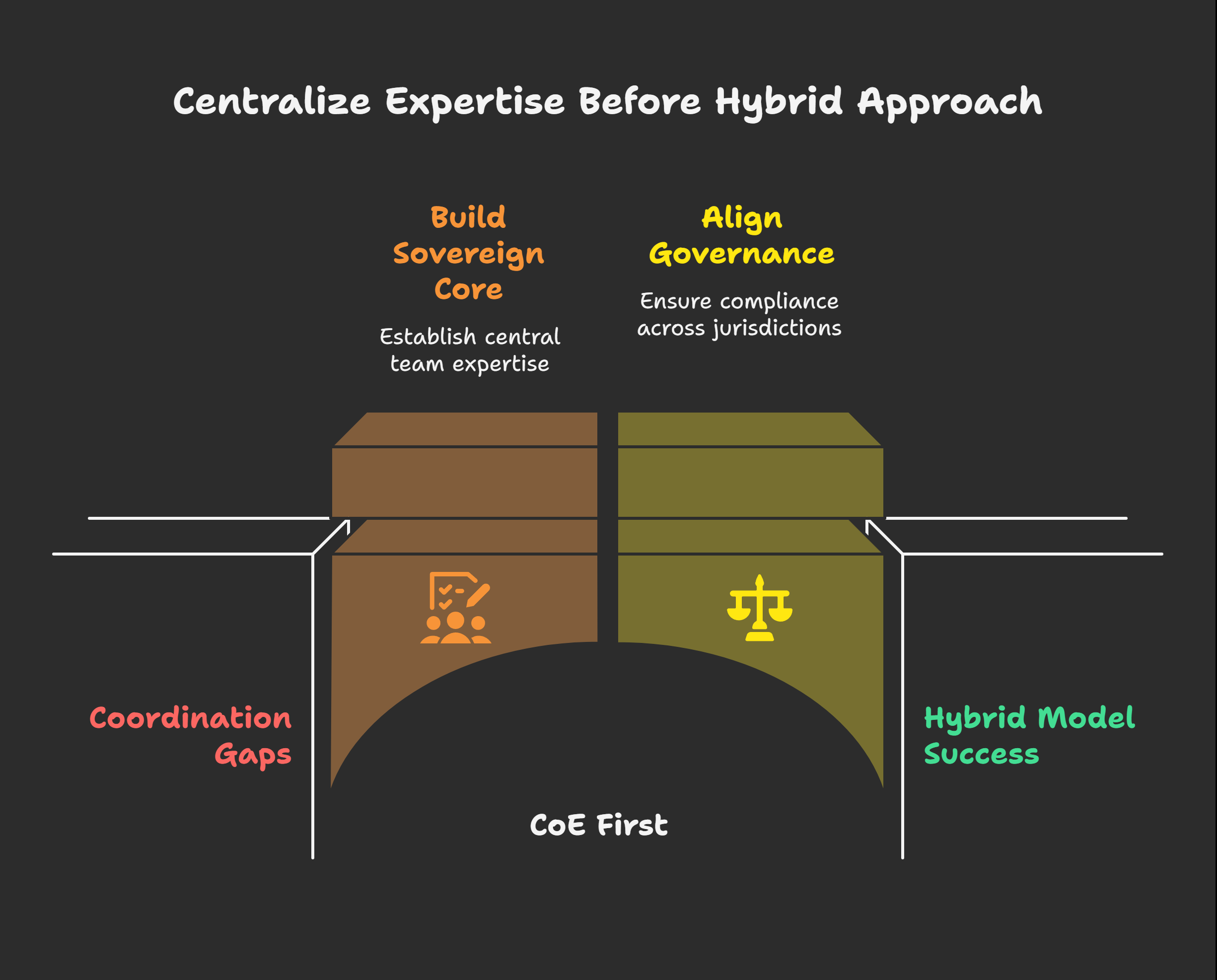

HSBC: Hybrid Promise, Governance Gaps

HSBC attempted a hybrid hub-and-spoke structure: central teams building credit and fraud engines, local units customizing models. It achieved technical successes — including advanced fraud detection through Decision Intelligence — but adoption slowed under the weight of coordination gaps.

The verdict is clear: CoE first, hybrid second. Without a sovereign core, distributed models struggle to align with governance, especially across jurisdictions.

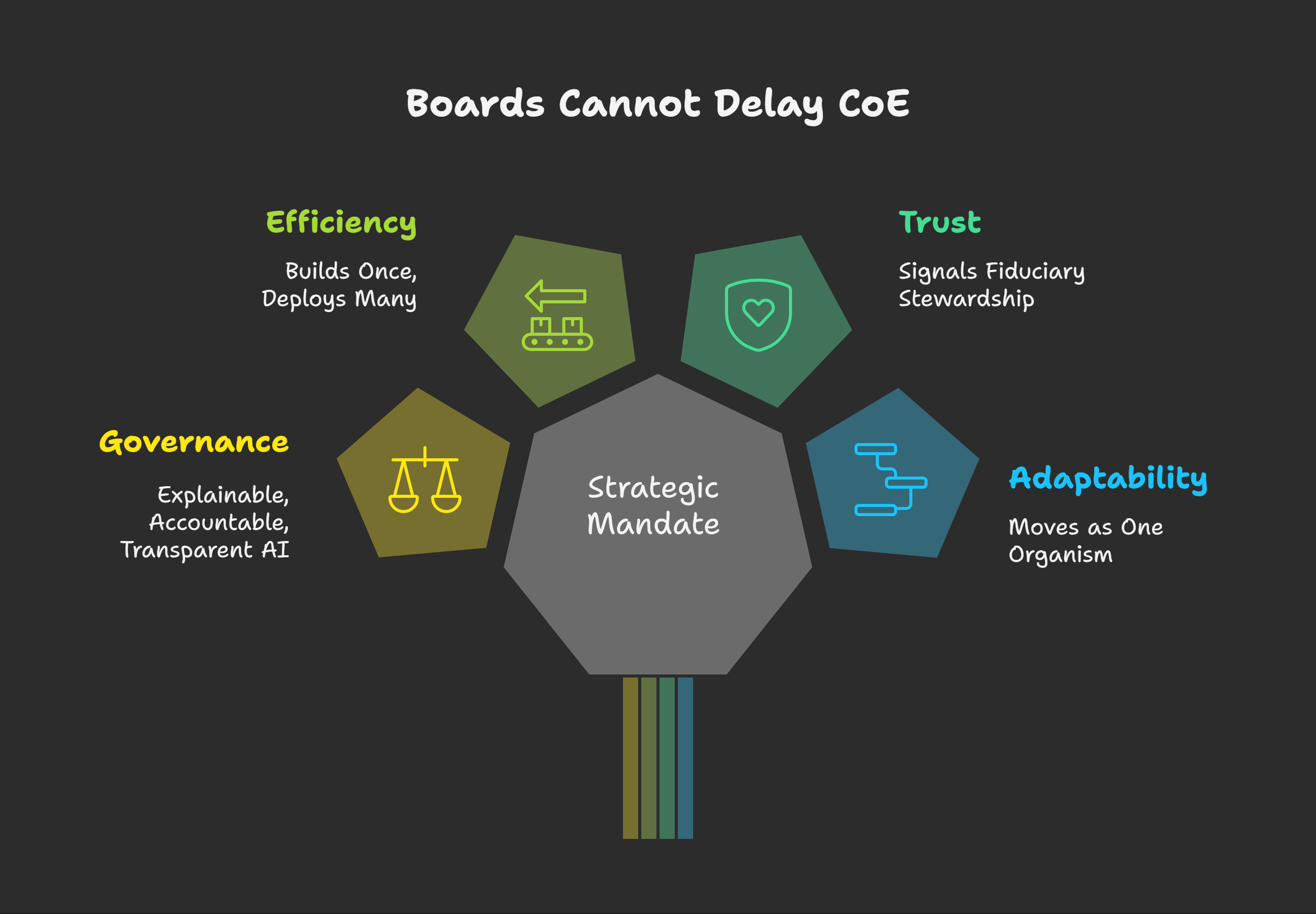

Why Boards Cannot Delay

For bank boards, a CoE is not a “technology project.” It is a strategic mandate. Four imperatives make delay untenable:

Governance – Regulators demand AI that is explainable, accountable, and transparent. A CoE enforces uniform standards, protecting brand credibility.

Efficiency – Instead of duplicating models across divisions, the CoE builds once and deploys many, compressing cost.

Trust – Clients measure banks not by how fast they adopt AI, but by how safely. A CoE signals fiduciary stewardship.

Adaptability – AI evolves weekly. Only a CoE ensures the bank moves as one organism, not scattered cells.

Investors, regulators, and clients will not accept AI chaos.

The misconception is that a CoE is defensive — a shield against regulators. In reality, it is expansive.

Once ING consolidated its models, it unlocked new capacity: AI-enhanced onboarding that compressed weeks into hours, real-time fraud detection safeguarding billions in daily transactions, personalized digital banking anticipating client needs before they voiced them.

These were not proofs of concept. They were enterprise weapons.

A CoE turns AI from a compliance expense into a growth infrastructure.

How to Frame the Mandate

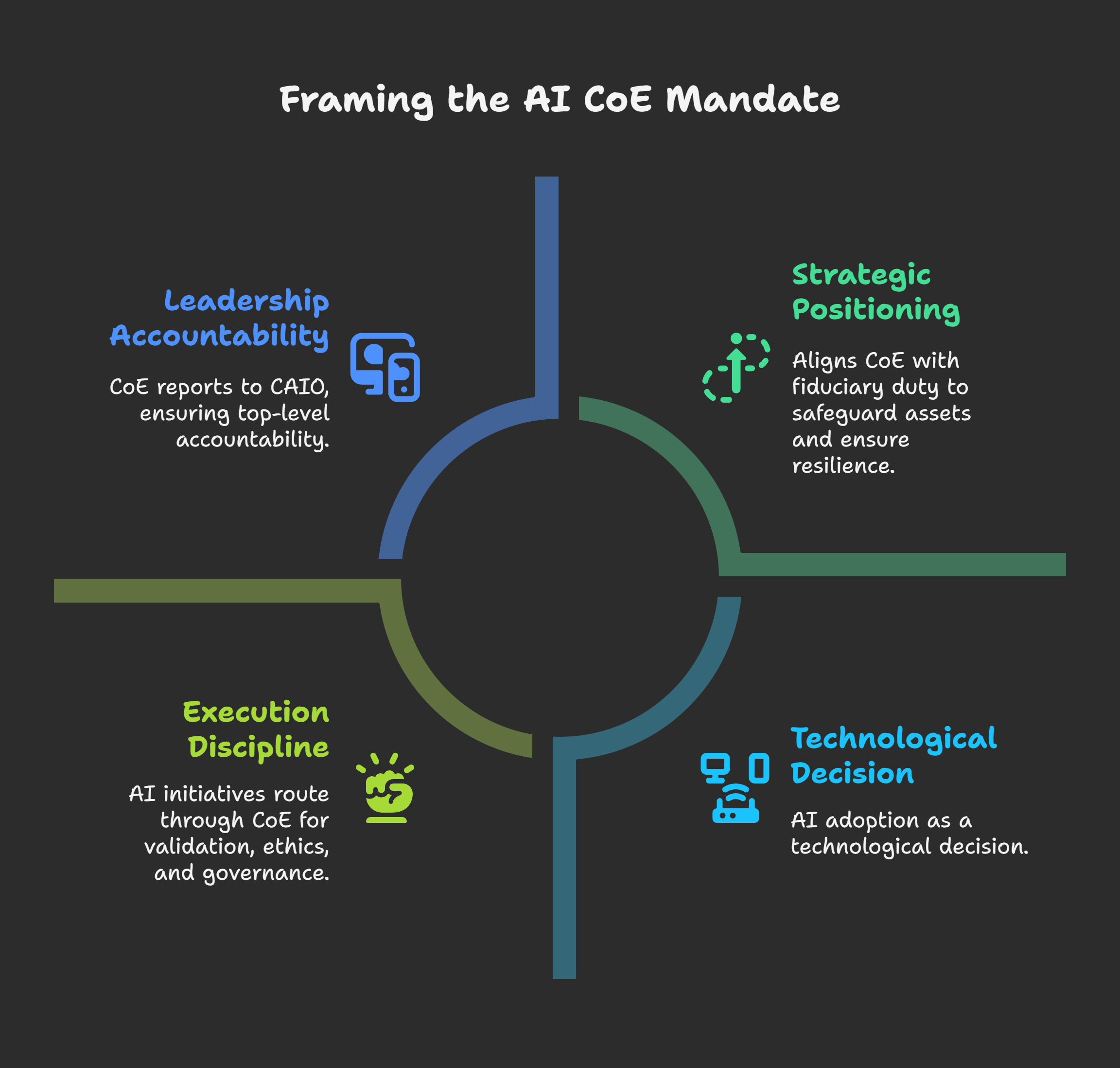

Boards should frame the AI CoE as fiduciary architecture, not IT. Three principles are non-negotiable:

Strategic Positioning: The CoE is enterprise infrastructure, aligned with the bank’s fiduciary duty to safeguard assets and ensure resilience.

Leadership: The CoE must report into a Chief AI Officer (CAIO) or equivalent — not buried in IT. Accountability must sit at the top table.

Execution Discipline: Every AI initiative routes through the CoE for model validation, ethical assessment, and governance.

This is not bureaucracy. It is clarity.

Why does this distinction matter? Because AI adoption in banking is not just a technological decision — it is an operating model shift where governance is the alpha.

Clients entrust capital across generations. Regulators enforce transparency across borders. Without a CoE, banks cannot meet either test. With one, they secure both.

That is why the CoE is not just operational necessity. It is fiduciary sovereignty.

The Way Forward

Banks cannot afford AI chaos. They need Centers of Excellence that centralize expertise, enforce governance, and accelerate scale.

The next decade will not reward the banks with the most AI pilots. It will reward the banks that build the calmest, clearest AI structures.

The Center of Excellence is that structure.

For boards ready to expand without strain, govern without resistance, and grow without noise, the path is not another experiment. It is sovereignty.

The instinct has been there all along: there is a better way — quieter, smarter, stronger. Now there is a structure to support it.

The Center of Excellence.